India's answer to fragmented claims process.

An ambitious protocol to solve the painful claims process.

I had my family member admitted for a surgery two years back. The hospital, the surgeon and his team did an excellent job. The surgery was successful and the long standing, years of pain had disappeared. Bags were packed and we were excited to get back home, but the insurance claim was not settled. This was a pre-approved surgery, well covered under the insurance plan.

Most of us have gone through the claims process. Patient is treated, the hospital is ready to discharge but the insurance claim is not processed. The waiting times are more painful not only because of wait times but more so, because of wanting to get home ASAP. The hospital lobby has a constant flow of agitated care-takers, wanting to know the status at every stage from pre-approval, sanction to settlement.

For cashless claims, there is waiting time for treatments to get approved. If not planned well, days go by without initiation of treatment. Now I make it a point to get approval before getting admitted to save time for everyone involved.

If the system struggles so much for in-patient (IP) treatment, think of the claims process for Outpatient (OP) one off consultations. Any decent clinic or hospital always has long queues. The entire claims process has to be super quick, less than a few minutes for consultations to carry on smoothly.

The Health Claims Exchange (HCX) protocol aims to solve this and is gunning for more

Improved patients’ claim related experience

Better visibility and tracking of claims

Reduction in claims processing cost

Newer innovative insurance products

There are multiple stakeholders involved in the process. Currently the process is manual. Documents are scanned and emailed. The reviews and approval takes hours and some time days.

So ride along to know who the stakeholders are, what is the scale of the challenge, what does the current insurance landscape look like, how does the protocol aims to solve it, how HCX builds on top of existing infrastructure, how it fits into the ambitious Ayushman Bharat Digital Mission (ABDM).

I will also cover what are opportunities in the space for startups, professionals and insurance providers.

The Stakeholders

The key reason why it takes so much time is mainly because there are several important stakeholders.

[Image Credit: hcxprotocol.io]

Providers: The hospitals and clinics that provide the care

Insurers: Health insurance companies and the Third Party Administrators (TPA). TPAs are intermediaries between the insurance provider and the policyholder and its key function is processing of claims and settlement

Regulator: The Insurance Regulatory and Development Authority(IRDA) of India is a statutory body under the jurisdiction of the Ministry of Finance, Government of India and is tasked with regulating and licensing the insurance and reinsurance industries in India.

Sponsors: A plan sponsor is an employer or organisation that offers a group health plan to its employees or members.

Patients: Not shown in the image above but the most important stakeholder. Patients and policy holders will only benefit if all of the above stakeholders co-ordinate and speak the same language.

The Scale Of Challenge

Our huge population, lack of coverage legacy and very little software adoption are challenges of enormous scale. Solving this will require innovation at policy level, building platforms, interoperability between all stakeholders and innovation by start-ups.

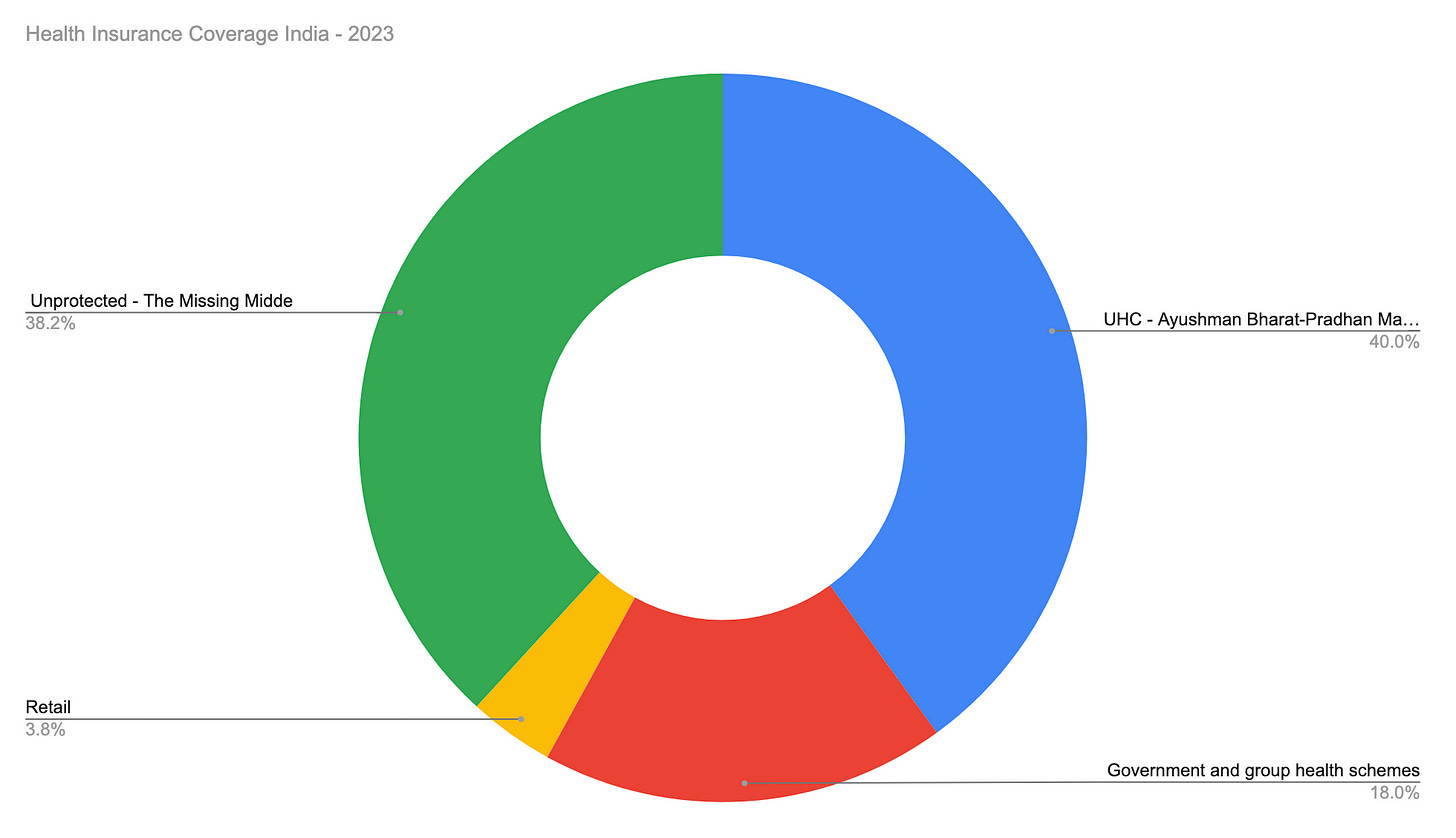

Insurance Coverage

Let’s start with looking at the population covered with insurance today. How it is likely to keep growing and how does this impact the architecture of the system.

Do the retail insurance numbers have uncanny resembles to tax payers? Looks like this is the formal workforce.

The missing middle, a huge 527 Million Indians don’t have health insurance.

Who is the missing middle?

Urban:

Rural:

The formal workforce has the ability to influence the missing middle. I have seen several close friends, relatives and families both in urban and rural India without health insurance.

The reason is simple. Affordability. Look at the insurance pricing below. We know the insurance cost of ~25K annual premium for any of the missing middle households is steep.

Showing them proof of your claims, helps them get on-board. This needs enormous awareness. The trust needs to be built with smaller transactions.

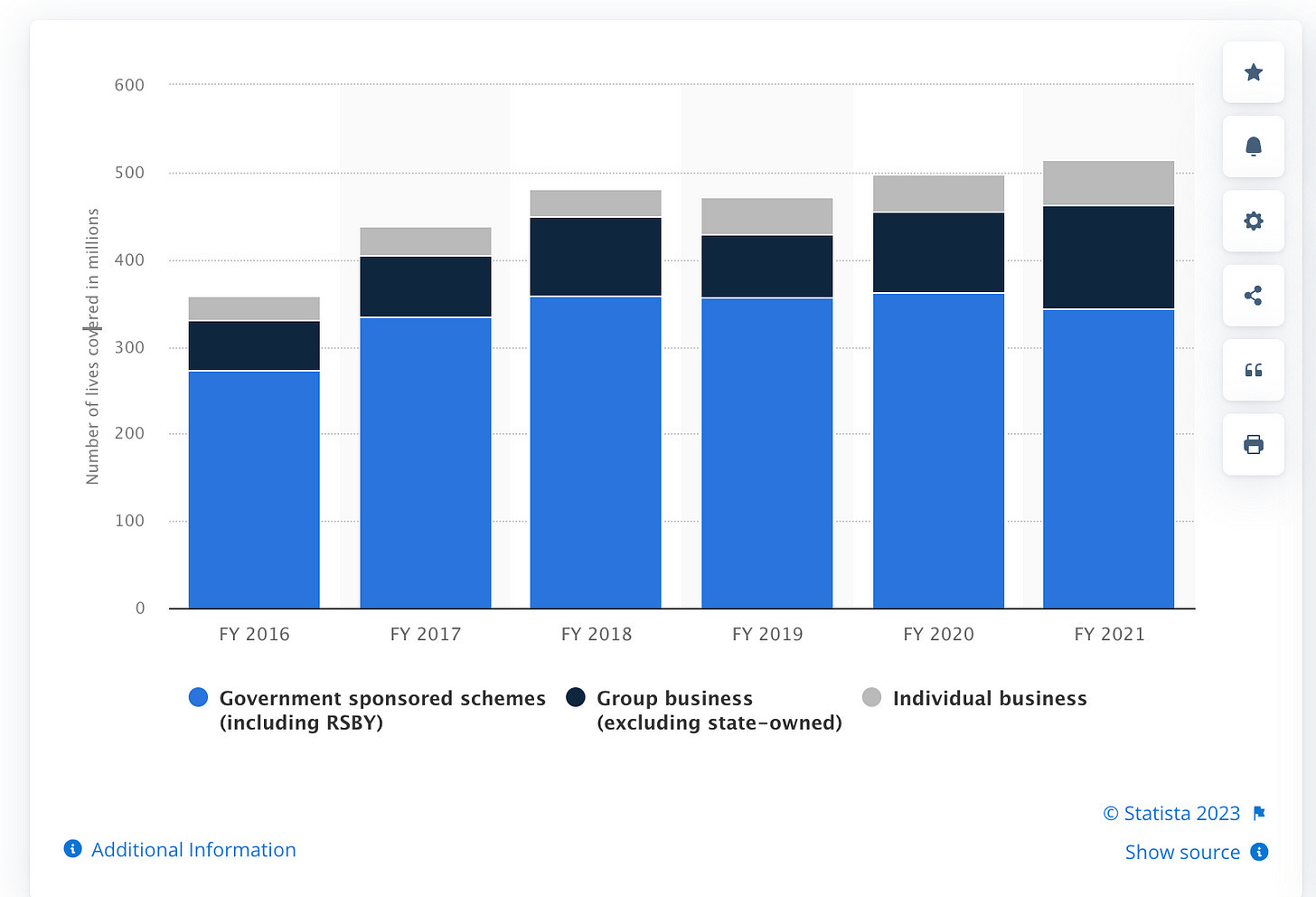

The penetration is bound to increase with more disposable income. See below the number of people with health insurance across India from financial year 2016 to 2021, by business type.

Fragmented Health Information Systems

There are ~37K hospitals in India, with 7.39 Lakh beds as per data uploaded by States and Union Territories on HMIS portal, status as on 20 July 2018.

The current state of interoperability with hospitals and outside leaves a lot to be desired. Solving digitisation is a priority for the hospitals however they have a bigger challenge of serving the patients, with such skewed beds to patients ratio. Digitisation is often outsourced to third party vendors adding additional complexity to adoption and solving key issues.

In my experience basic API integration that should happen in weeks in other industries takes several months with current hospital systems. This is a pretty big challenge as well as a great platform building opportunity.

How does HCX aim to tackle this?

The HCX protocol has very well thought out

Technical Specifications for building technology backbone for Health Claims Data Exchange

Domain Specifications for agreement on formats for data exchange

Business Policy Specifications provides guidelines for key business processes like on-boarding, de-boarding, dispute resolution, SLAs, fees and ratings.

Check the complete specification to know more. All of the development is Open source at HCX Project.

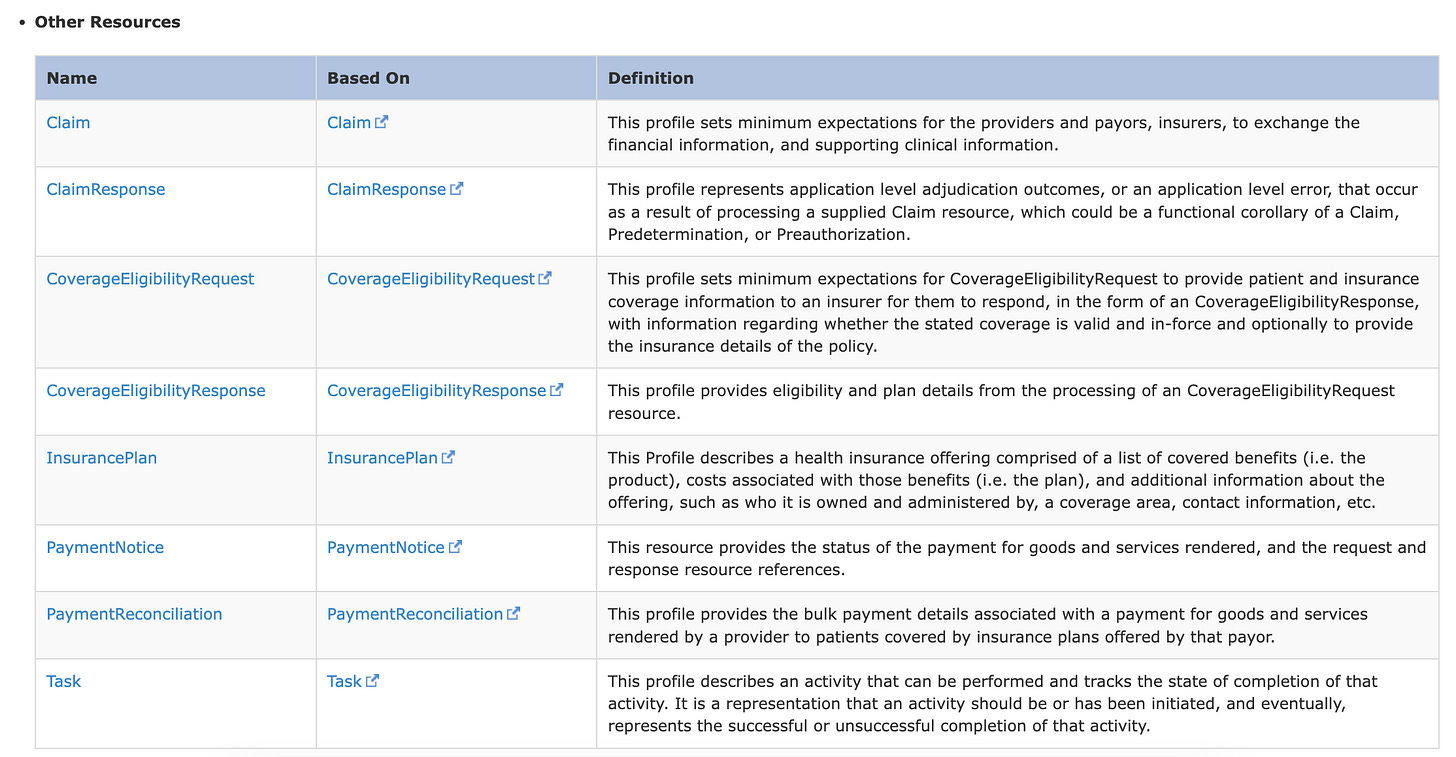

HCX builds on top of Fast Healthcare Interoperability Resources (FHIR)

The FHIR standard is a set of rules and specifications for exchanging electronic health care data. The standard is seeing a rapid adoption across the world. India’s has opportunity to leapfrog legacy standards. HCX is definitely doing this right with FHIR adoption

For all the stakeholders to speak a common language, to automate the workflows HCX uses custom FHIR profiles.

Key use-cases supported are:

Get provider/payor details

Eligibility check

Pre auth request flow

Claims request flow

Payment notification

Payment acknowledgement

Search/fetch claims data for status checks, regulatory compliance, etc.

Check the FHIR Implementation Guide here. This provides a way for all stakeholders we discussed above to speak the same language.

How does this relate to Ayushman Bharat Digital Mission (ABDM)?

The ABDM Stack is a bold and futuristic initiative just like UPI. Look at the scale of challenges above, it will take more years and industry collaboration on a bigger scale. As you can see, HCX is a key component of the stack.

Although in the short term HCX efforts may sound unrealistic but in the long run it has immense potential to unleash health care innovation. Given a 2-5 year horizon, this has potential to unleash health care innovation that exceeds global norms as with UPI.

Opportunities in the Space

Insurers

There is already a lot of innovation in space. The Aarogya Sanjeevani Health Insurance Plan by the Government aims to tackle this by standardisation and simplifying offering.

This has resulted in a lot of new policy offerings by private insurance players.

Claims

The number of claims are quite low as can be seen below. The need for the transformation is only bound to increase as the health insurance penetration increases

Nearly 4.5 crore Indians got Covid in the last two years since the pandemic struck while around 5.30 lakh of them lost their lives. However, just 27 lakh people availed insurance claims worth `24,000 crore, as per Government data.

It comes amid a recent survey that found that almost 50 per cent of patients feel that the long waiting time for approvals is the biggest pain point while filing for the insurance claim and nearly 60 per cent of patients are delaying treatments because of lack of health insurance.

https://www.dailypioneer.com/2022/india/27l-people-availed-health-insurance-claims--data.html

Startups

There is already an incentive scheme in place. The impact of monitory incentive needs to be seen. However I believe there is a bigger role for startups to play.

Data for insurance innovation. Age and Health check-up are only two data points that are used to evaluate insurance currently. The only real pricing indicator for the majority of policy sales is Age. Shouldn’t the premium be based on other health indicators like patient medical history, vital signs, and regular monitored data?

Integrations: The Hospital Informations Systems [HIS] market is quite fragmented in India. There are no large players like the western markets. Several of these are on-prem. Each of these fragmented players have their custom data models, non standard APIs. With so many stakeholders involved no app innovation can happen without good integration players. A big opportunity in the space is to ingest non-uniform data sources and output a standard complaint data stream.

App Innovations

Claim Process Tracking: Will patients be happy to track their claims with the same ease as food delivery?

Treatment Coverage: How about the ability to find out if a medical condition is covered in your policy by a simple search?

Hospital Portability: How about getting treated at a hospital of your choice? The current system forces you to look at TPAs Network Hospital first before any other more important criteria.

New Age HIS Systems: Globally the HIS systems are complex software with not so great UI/UX. India has a big opportunity to build modern and scalable HIS apps on the ABDM platform

Developer, Product, Regulatory, QA Professionals

India has a huge talent pool with extensive experience in building health technologies for the world. With so much innovation on the horizon, developers, product managers, regulators and QA professionals will have great opportunities to lead the innovation.

In-fact the team at HCX is looking forward to receiving help. The specs are open-source and getting involved as with any other open source initiative should lead to tremendous professional growth and connections. I plan to cover the current state of Ayushman Bharat Digital Mission(ABDM) in my next post. Subscribe for more.

I will leave you with a photo from FHIR community meet-up that happened on December 4, 2023 which was a big inspiration for this deep dive.

References

https://www.niti.gov.in/sites/default/files/2021-10/HealthInsurance-forIndiasMissingMiddle_28-10-2021.pdf

https://www.nrces.in/preview/ndhm/fhir/r4/profiles.html FHIR Profiles Created for ABDM

https://abdm.gov.in:8081/uploads/Digital_Health_Incentive_Scheme_550e710e09.pdf

https://abdm.gov.in/

https://docs.hcxprotocol.io/